Land auction 27th January at 4.30pm

Join us on Saturday 27th January at 4.30pm at the Rye Hotel. 7 blocks of land going under the hammer, starting from $390,000 In room land auction Saturday 27th January

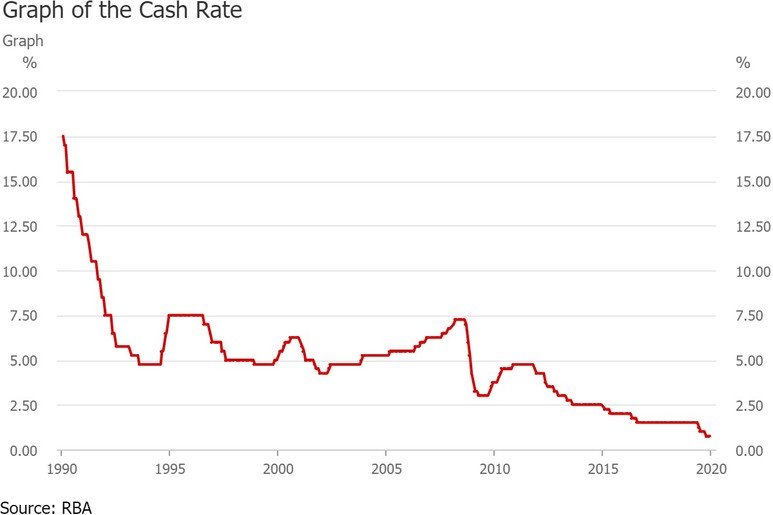

Throughout the course of 2019, the Reserve Bank of Australia (RBA) has decreased the official cash rate to a historic low of 0.75%. But what actually is the cash rate and how does it affect current property buyers?

The cash rate is the overnight interest rate set by the RBA, which determines the cost of borrowing and lending between banks. This interest rate sets the benchmark for the cost of debt (or borrowing) in the economy.

Since October 2010, the official cash rate has steadily decreased, simultaneously decreasing the cost of debt. This is because a lower cash rate reduces the cost of bank funding. This in turn increases banks confidence in their ability to lend money to consumers, and, therefore, they are able to offer lower interest rate loans. The same holds true in reverse; as the cash rate increases, banks are likely to increase the interest rates associated to various loans, as the cost of bank funding increases. This is referred to as monetary policy. It is important to note that the cash rate does not dictate the interest rates set by banks, but rather serves as a guide.

As the RBA continues to cut the cash rate, the interest rates associated to various home loans have been decreasing. This means, from a finance perspective, it is the ideal time to consider taking out a home loan.

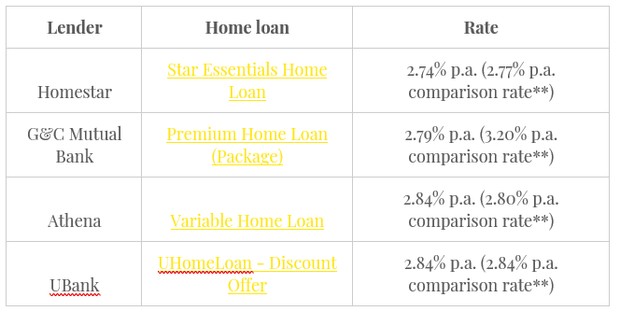

Below are three of the lowest variable rate home loans discovered by the Money Saving Zone (Mozo):

Although interest rates may be at an all time low, there are a number of other factors you should take into consideration before taking out a mortgage. Such factors include:

These are all questions you should be asking yourself before purchasing a home. If you require any further advice or assistance on this topic, please feel free to contact our office via the portal below.

Join us on Saturday 27th January at 4.30pm at the Rye Hotel. 7 blocks of land going under the hammer, starting from $390,000 In room land auction Saturday 27th January

The question of “should I rent or should I buy?” is a timeless dilemma. Below are a list of pros and cons that can help you make a more informed decision. Renting – the pros 1. Freedom to relocate As a tenant you have the freedom to chose what you … Read more